Charles Spinelli Throws Light on the Calibration of Human Interruption Policies by Workers’ Compensation Insurance

188 ViewsWorkers’ compensation insurance stands as one of the most quietly transformative frameworks within modern employment systems, according to Charles Spinelli. This structure was originally […]

Key Metrics to Compare Digital Personal Loan Options

196 ViewsThe financial landscape has shifted dramatically over the last decade. Gone are the days when you had to visit a physical bank branch, wait […]

Men Need to Know Foods That Can Support and Harm Testosterone Levels – A Guide from Evan Bass Men’s Clinic

851 ViewsTestosterone is among the most essential hormones in men’s lives. It is responsible for muscle growth, mood, and energy, aside from sexual health. Food […]

The Amazing Benefits Of Personalized Bottles

1,538 ViewsDrinking enough water is more crucial than ever in the fast-paced world of today. A customized bottle accomplishes this goal while also providing a […]

Essential considerations about CBD oil price in India

1,869 ViewsCBD oil is gaining momentum in India as a wellness supplement for issues like anxiety, sleep disorders, chronic pain, and inflammation. But for many […]

Break Into Data Analytics: Find The Perfect Course in Bangalore

1,511 ViewsMultinational, startup, and mid-sized companies seek data analytics expertise for their organizations. These professionals can design new customized tools according to the requirements, handle […]

Why is Everest Base Camp so popular?

1,584 ViewsEverest Base Camp (EBC) is one of the most famous trekking destinations around the world, attracting trekkers and adventure seekers from every part of the […]

How Recruitment Consultancies Drive Talent Acquisition in Abu Dhabi Job Market

1,671 ViewsIn the past 10 years, the job market in Abu Dhabi has grown by offering businesses with scintillating professionals across many degrees. Specialized recruitment […]

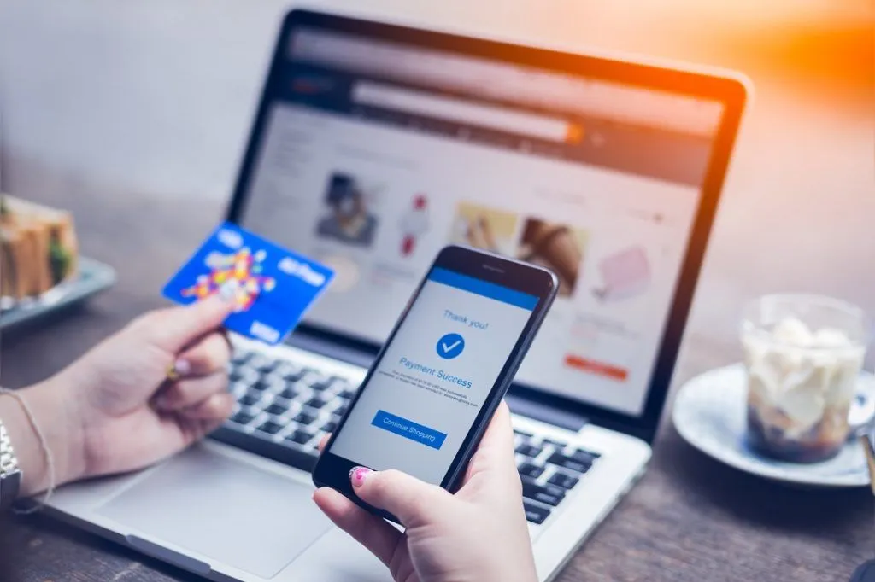

Easy online payment for your customers

1,543 ViewsLooking for ways to streamline the online payment process for your customers? In today’s rapid digital world, convenience and efficiency are important. By using […]

The Health Benefits of Sushi: Why Nazcaa is Your Go-To for Fresh Sushi and a Great Rooftop Experience in Dubai

1,466 ViewsSushi, a Japanese culinary masterpiece, has evolved over centuries to become a global sensation. Its delicate balance of flavors, textures, and artistic presentation has […]